Do Australian CFD providers have contracts with unfair terms?

Summary: Every year, Australian Contract for Difference (CFD) providers make hundreds of millions in trading revenue from Australian clients which according to ASIC are a "combination of net client losses and fees and costs charged to clients." And over 70% of Australian CFD retail clients are net losers each year; thus over the life of an account this proportion of net losers would be even higher - likely over 90%.

Thus, as you might expect given such wealth extraction, each year, thousands of Australians complain about unfair losses relating to CFDs. Complaints must first be submitted to the provider with only a minority of clients pursuing them further with the Australian Financial Complaints Authority (AFCA).

However, any unfairness in CFD providers' standard business model is rarely investigated, let alone redressed by the AFCA complaint process. The AFCA appears to rely on the assumption that the terms and conditions clients accept when they sign up with a CFD provider are legal, thus if the action being complained about is within the terms (no matter how tilted toward the provider), it cannot make a decision in the client's favour.

A case I have with the AFCA against a CFD provider (IG Markets Australia) has come down to this: IG Markets actions are supposedly within the terms I "accepted" (i.e. ticked a box saying I'd accepted all terms in a lengthy, linked PDF document that was deliberately unclear about the actual margin call process and existed to provide carte blanche protection to any actions IG Markets took in service of its interests).

My position is that key terms in IG's CFD agreement relevant to my case are clearly unfair as defined by Australian consumer law. Only a court can formally determine whether a contract term is unfair, but these terms have not been assessed by any Australian court as far as I am aware.

In this post, I will demonstrate how various IG terms are unfair, unreasonable, impossible, obscure or contradictory. I will publish any response from IG Markets to these assertions their terms are unfair (to date, they have refused to consider some of their terms could be found illegal if tested in court.) I invite IG Markets to take me to court to test this if they are so confident.

Cases of specific financial loss are handled by the AFCA. But "ASIC is responsible for enforcing the unfair contract terms law in relation to financial products and services" (i.e. the broader regulation affecting all future business practice.) Hence, I will also be submitting a complaint to ASIC as advised on its website and will provide as much time and effort as needed to assist with any systemic remedy including having this reviewed by a court. Given the magnitude of the losses incurred by Australians each year, it is a travesty that the issue of unfair terms in CFD provider contracts hasn't been addressed so far.

Details:

Update Nov 2020: The seven month AFCA "investigation" of my complaint concluded that IG Markets did not act unfairly in any way according to Australian law and that "there is no significant imbalance in the parties’ rights and obligations."

The AFCA "investigation" of my complaint committed every type of error you can imagine:

- They got various salient facts wrong despite my having established them with written evidence (e.g. the facts about the margin call timing and triggering).

- They refused to quote a single aspect of my detailed complaint and instead disingenuously reduced it to a couple of sentences they wrote themselves. E.g. They simply stated that I asserted IG's margin call terms are unfair without quoting and discussing any of the very specific points I made establishing why they are unfair (see below).

- The AFCA assessment relies on motivated reasoning to defend the patently unfair CFD practices it has helped protect year after year despite being inundated with complaints from Australian citizens getting burned by this extractive industry.

I could go on in detail to scrutinise every failing of the AFCA's written assessment but have concluded that the AFCA cannot be relied upon to investigate such complaints fairly or properly. If at some point some independent review of the AFCA takes place, I will be using their written assessment and details of their actions in this case as evidence of their many failings.

However, I will demonstrate with just one example how absurd the AFCA conclusion of no unfairness is. Here is a quote from the AFCA assessment:

<<

On 5 March 2020 at 1:51AM, the financial firm says it sent a margin call notification to the complainant. The financial firm has provided a copy of it. A margin call warning is initially trigger when 75% (=1,855.51/ 2,005.42 X 100 is greater than 75%) of the account equity is used in meeting the account’s margin requirements. The complainant has not indicated whether he received this margin call warning, and in any event, the complainant says he was asleep at the time.

>>

But the reality (that the AFCA chose to hide) is that IG Markets opened my position at 1:50am!! Then placed my position in "default" (according to their unfair terms and thus subject to close-out without notice at any time henceforth) less than 30 seconds later!

Any independent, reasonable person would conclude this is a gambling product scam not an investing product as IG Markets and the CFD industry purport to be.

Any unbiased person would wonder how an investing product can be legally designed such that trades can be opened and then immediately placed into "default" subject to liquidation at any moment and without notice?

The reality (which the AFCA deliberately obfuscates in its assessment) is that the CFD industry intentionally designed the product this way. With 20 to 1 leverage and a 75% account equity threshold it only takes a 1.25% price movement to put an account in default if the CFD provider fails to ensure the total account equity limits have sufficient buffers in place.

The AFCA position essentially claims that this situation is clearly and transparently disclosed to all new customers, is not unfair, and there is no imbalance between the rights and obligations of the customer versus the CFD provider. Any independent person can see this is totally rigged to protect the CFD provider at the expense of the client and also maximise the CFD provider's capacity to make profits via allowing trades to be placed with essentially zero account equity buffers in place.

I explained this very clearly to the AFCA Case Manager via email (see below). Tellingly, they completely ignored this and didn't reply via email and deliberately ignored this in their written assessment. This speaks volumes about how the AFCA currently functions and the massive reform needed to this agency.

Finally, the AFCA assessment defends the current CFD practices as fair, reasonable and not imbalanced but fails to mention that ASIC has found them not to be and is using its product intervention powers to force changes to leverage (reducing from 20 to 1 to 5 to 1 for equities like Tesla) and other aspects to shift the current unfair balance of rights and obligations between consumers and CFD providers.

https://asic.gov.au/about-asic/news-centre/find-a-media-release/2020-releases/20-254mr-asic-product-intervention-order-strengthens-cfd-protections/

I don't think ASIC goes anywhere near enough in its reform and the next logical step is to gather evidence to get the CFD industry shut down to most retail clients in Australia. More to come on this as I will detail my efforts to collect this evidence.

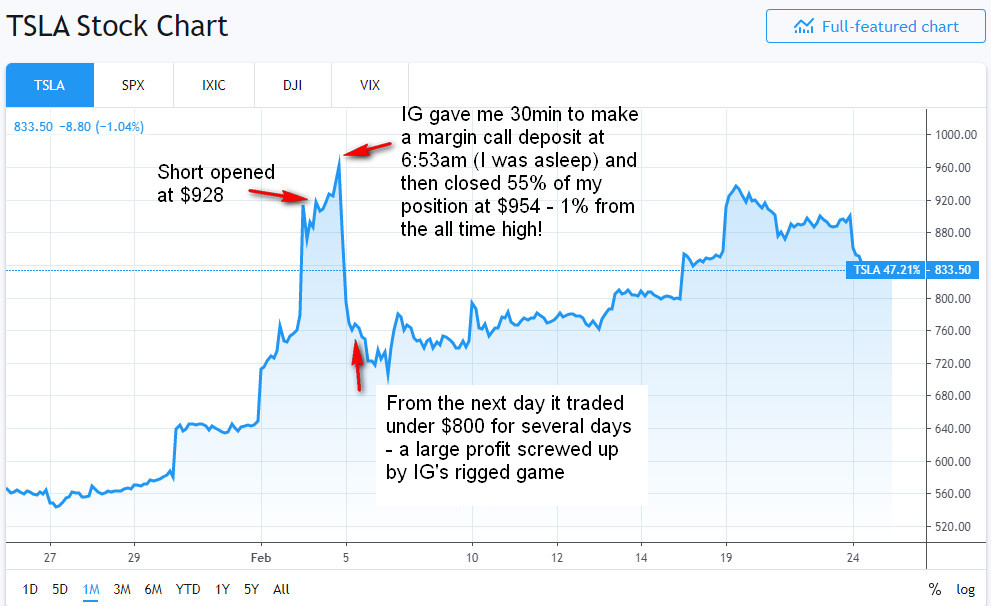

1. My complaint: No reasonable opportunity given to me to fund a margin call and a trade was partially-closed by IG Markets using an Automated Close Out Process not disclosed in its Customer Agreement. This ultimately cost me $17,803.

IG Markets Australia opened my short limit order position in TSLA at 1:50am, and it's Automated Close Out Process sent me a margin call email at 6:53am, and then automatically closed out 55% of my position 30 minutes later at 7:23am. I was asleep the whole time!!

2. What are Unfair Contract Terms under Australian law?

<<

Meaning of 'unfair'

A term in a standard form consumer contract is 'unfair' if:

- it would cause a significant imbalance in the parties’ rights and obligations arising under the contract

- the term is not reasonably necessary to protect the legitimate interests of the party that would benefit from its inclusion

- the term would cause financial or other detriment (e.g. delay) to a consumer if it were to be applied or relied on.

Transparency of the term

A term is considered to be 'transparent' if it is:

- legible

- expressed in reasonably plain language

- presented clearly

- readily available to any party affected by the term.

>>

3. A summary of IG Markets and my position regarding the complaint and the terms in the Margin Trading Customer Agreement (MTCA)

- IG Markets acknowledges its Automated Close Out Process closed out 22 of 40 units in my TSLA short position. It does not dispute this caused an immediate $863.27 loss; nor can it dispute that if I'd been allowed to fund the margin call my profit on this trade would have been $16,940 greater.

- IG Markets claims its MTCA terms allow for it forcing closure of client positions with 30 minutes notice even while they are asleep, and that I have accepted its terms by ticking the box when becoming a client, thus I am responsible.

- My position is that the relevant terms would likely be found to be Unfair Contract Terms (thus illegal or not binding) if tested in court or via a regulatory authority:

a. It's terms do not advise of a specific Automated Close Out Process let alone a timeframe of 30 minutes between notification and close out - which they easily could. Instead, they simply assert payment is due "immediately" which is either impossible or an undefined timeframe.

b. It's terms do not advise of a specific notification process for Automated Close Outs (that an email will be sent giving 30 minutes notice and positions fully or partially closed if still beyond margin limits). Instead, the terms say the positions can be closed "whether or not we contact you" and that the client is responsible for continuously monitoring their margin position by logging in or phoning in (unfeasible as clients have to do other things including sleep!)

So essentially IG's terms say they are providing a Margin product which requires manual human action to fund margin calls by depositing funds (or modify the position exposure) but can force closure of client positions immediately and without providing any notice.

Any reasonable person would conclude that a Margin product requiring manual human action to address margin calls requires a reasonable timeframe and process for clients - it absolutely cannot be immediate (it's impossible to be aware of a margin call and transfer funds in seconds), of undefined timeframe (you need to be advised how long you have), or without notice (that's unfeasible as people can't be expected to be logged on constantly without ever sleeping). Indeed, any legitimate margin product offered with fair terms is done so with precise, accurate and concise language:

As you can see in the CommSec example, it's simple and very concise when you actually are offering a legitimate, fair margin product. When you are offering an unfair margin product skewed to serve the interests of the CFD provider, you refer to various sections of multiple lengthy documents that simply provide the broadest discretion to the provider and never spell out to the client the timeframes, notification or close out processes that actually apply.

Unfortunately for IG Markets, its current Agreement terms are in parts impossible, undefined, unreasonable, contradictory or illegitimate as defined by Australian law on unfair contract terms.

I have saved PDF copies of all IG Markets Australia Customer Agreement and PDS documents and there is no use in them making changes to retrospectively address their failings below. Should this proceed to a more formal process involving lawyers, I will compile full excerpts of the terms in the various documents to fully substantiate the summary below which I have kept concise for my AFCA complaint and initial ASIC complaint.

4. IG Markets Customer Agreement terms have not been written to transparently disclose the actual process and timeframes for notifying of and resolving margin calls. They have been written to provide IG Markets carte blanche (especially in a dispute) to protect its profits and minimise its exposure/liabilities at the expense of customers legitimate, reasonable interests.

The key section IG Markets has relied on in our dispute is below:

<<Section 15; pg 9

(2) You also have a continuing Margin obligation to us to ensure that at all times during which you have open Transactions you ensure that your account balance, taking into account all realised and/or unrealised profits and losses (“P&L”) on your account, is equal to at least the Initial Margin that we require you to have paid to us for all of your open Transactions. If there is any shortfall between your account balance (taking into account P&L) and your total Initial Margin requirement, you will be required to deposit additional funds into your account. These funds will be due and payable to us for our own account, immediately on your account balance (taking into account P&L) falling below your Initial Margin requirement...

>>

<<Section 15; pg 10

(3) Details of Margin amounts paid and owing by you are available by logging on to our Electronic Trading Services or by telephoning one of our employees. You acknowledge: (a) that it is your responsibility to be aware of, and further that you agree to pay, the Margin required at all times for all Transactions that you open with us; (b) that your obligation to pay Margin will exist whether or not we contact you regarding an outstanding Margin obligation; and (c) that your failure to pay any Margin required in relation to your Transactions will be regarded as an Event of Default for the purposes of Term 17.

>>

<<Section 15; pg 10

(6) We are not under any obligation to keep you informed of your account balance and Margin required (i.e. to make a ‘Margin call’) however if we do so the Margin call may be made by telephone call, post, email, text message or through an Electronic Trading Service. The Margin call will be deemed to have been made as soon as you are deemed to have received such notice in accordance with Term 14(10).

>>

But if you refer to Point 2 of this blog post where I have documented what Unfair Contract Terms are under Australian law, it is obvious the terms above are unfair (imbalanced, not reasonably necessary, cause financial detriment to the consumer, and are not transparent.)

- Customers cannot possibly monitor their margin position continuously by looking at a screen or calling IG every 10 minutes and not a single person does. Legitimate margin call processes depend on a clear notification process and specific timeframes given to address the shortfall.

- While mentioned in its PDS, there is no term I accepted in the Customer Agreement that mentions (let alone describes) the Automated Close Out Process - which closes out trades 30 minutes after the margin call email at any time of day or night.

- Neither the terms quoted above or any other part of the Customer Agreement specifies the actual timeframe (30 minutes) that is used by the Automated Close Out Process and can be triggered at any time of day or night.

- Customers may well be willing to accept terms that cover the provider of a product when exceptional events occur (e.g. email system fails, extraordinary market circumstances) but only if they are confident they understand the normal operation is fair enough - in this case the Automated Close Out Process being clearly described in the Customer Agreement inclusive of the 30 minute timeframe. But it was left out so that the unfair carte blanche approach (to maximise IG Markets discretion and rights and place all obligations on the customer) could be applied without confusion or contradiction.

5. IG Markets Customer Agreement states margin call shortfalls must be paid "immediately" but immediately is never defined, instantaneous manual payment or modifying position exposure is impossible, and a separate section of its Agreement relating to payment refers to it being due the "same day"

<<Section 11; pg 20

Payments

Every payment to be made by a Party under these terms shall be made in same

day (or immediately available) and freely transferable funds to the bank account

designated by the other Party for such purpose.

>>

6. IG Markets states margin call payments are due immediately. But margin payments have to be paid manually into IG's account including by bank transfer with manual Proof of Payment screenshots if needed. "Immediately" is thus impossible and inaccurate.

<<Section 15; pg 10

(4) Margin payments must be made in the form of cleared funds (on your account with us)

>>

As noted with the CommSec example (next business day), legitimate margin call processes specify feasible timeframes for the payment methods agreed as accepted.

Common sense dictates that if IG Markets accepts a payment type for margin calls (e.g. bank transfer with manual proof of payment screenshot emailed afterwards) then a feasible specific timeframe must be allowed and disclosed before forcing closure of a trade.

7. IG Markets Customer Agreement terms it relies on in disputes are contradicted by other statements on its website or information channels (e.g. video, tutorials, etc)

As just one example, here is what its website says in clear terms about how "Maintenance Margin" works: it's as the customer expects - IG Markets requests from the customer extra margin. It does not expect the customer to stay continuously looking at the margin position on their device screen indefinitely or phone IG every 10 minutes. As soon as a margin call is triggered, it does not say instantaneous (within a minute) transfer of funds or reduction in position exposure is required.

A notification is expected and, consequently, a clear notification process and specific timeframe till IG closes the position needs to be described and understood by all customers before they trade.

<<

Maintenance margin

The maintenance margin, also known as variation margin, is extra money that we might need to request from you if your position moves against you. Its purpose is to ensure you have enough money in your account to fund the present value of the position at all times – covering any running losses.

>>

Comments

Post a Comment